Last updated:

Author

Jimmy Aki

Author

Jimmy Aki

Share

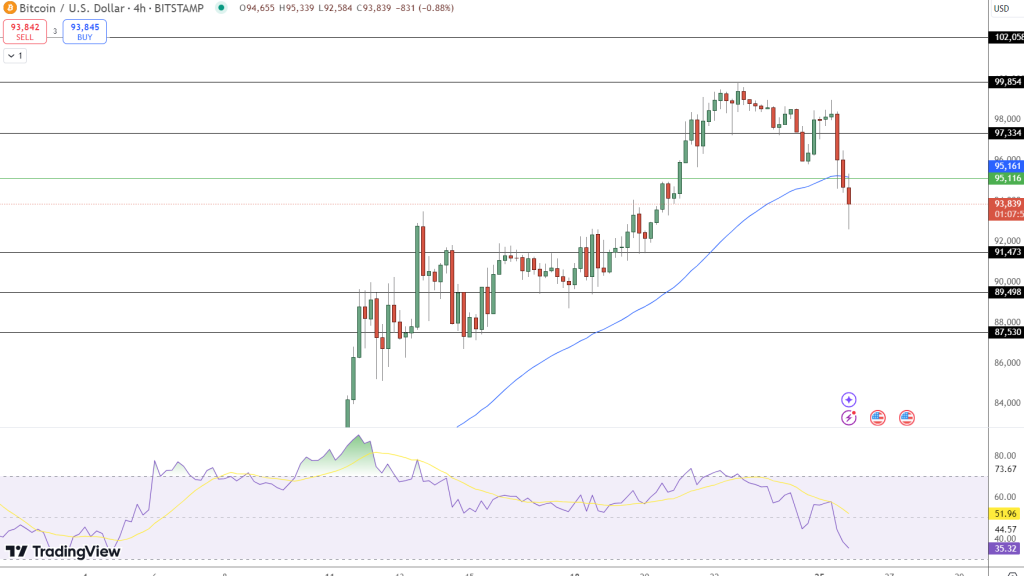

India’s Financial Intelligence Unit (FIU) took decisive action to recover $345 million in Goods and Services Tax (GST) from seven foreign crypto exchanges, including Kraken, Bitfinex, and MEXC Global, operating in the country.

This enforcement measure comes after several warnings issued to these exchanges regarding their failure to comply with India’s tax laws.

The exchanges involved, such as Kraken, Bitfinex, MEXC Global, Huobi, Gate.io, Bittrex, and Bitstamp, were banned from offering cryptocurrency services in India.

As part of the regulatory process, these platforms will now need to demonstrate compliance with Indian financial regulations, specifically the Prevention of Money Laundering Act (PMLA).

Foreign Exchanges Face Regulatory Hurdles in India

According to reports from the Economic Times, hearings will soon determine whether these exchanges can resume operations in India.

The exchanges will need to present their cases, showing compliance with the PMLA and demonstrating that they can fulfill the reporting obligations required under Indian law.

However, compliance with these regulations alone will not guarantee their return to the Indian crypto market. The exchanges must also pay fines, with the amounts to be determined based on their submissions during the hearings.

The FIU seeks to recover approximately ₹2,900 crores, equivalent to $345 million, in unpaid GST liabilities.

The Indian government has focused on recovering these taxes due to the exchanges’ failure to pay GST on transaction fees collected from Indian customers before being banned from operating in the country.

Earlier this year, the FIU asked Binance to pay $86 million in GST and a $2.25 million fine to resume its services in India.

These foreign entities are subject to the same GST rules as Indian businesses. This means they must register under India’s GST framework and pay taxes on services provided to Indian clients, just as domestic exchanges do.

India’s Strong Crypto Adoption and Future Outlook for Foreign Exchanges

Amid these regulatory hurdles, India’s leadership in global crypto adoption remains undisputed.

According to the Chainalysis 2024 Global Crypto Adoption Index, India ranks first among 154 countries in terms of cryptocurrency usage, even with a 30% crypto capital gains tax and a 1% tax deducted at source (TDS).

India’s crypto ecosystem has continued to operate despite these challenges, driven by activity on centralized exchanges, decentralized finance (DeFi) platforms, and peer-to-peer trading.

However, the introduction of strict tax measures in recent years has driven some Indian investors to international exchanges, where tax regulations are often less stringent.

In response, India’s GST authorities have begun considering sending notices to other foreign exchanges to ensure comprehensive compliance within the sector.

Earlier in September, reports suggested that the FIU reviewed registration requests from four additional foreign crypto exchanges, with two expected to receive approval to operate in India by the end of the 2025 financial year.